The Best Hotel Credit Cards for Budget Chains Are NOT What You Think

Signing up for credit cards through partner links earns us a commission. Terms apply to the offers listed on this page. Here’s our full advertising policy: How we make money.

Update: One or more card offers in this post are no longer available. Check our Hot Deals for the latest offers.

If you read travel blogs with any frequency you’ve seen the glorious hotel pictures and trip reports. Those iconic Park Hyatts, decadent Conrad resorts, and fancy Ritz-Carlton locations are on many of our bucket lists! And it’s for good reason – it’s easy to get massive value from your points when you redeem them for luxury stays like this, from cards like:

- Chase Sapphire Preferred Card or The World Of Hyatt Credit Card for Hyatt stays like Park Hyatt or Andaz

- Hilton Honors American Express Surpass® Card or The Hilton Honors American Express Business Card for Hilton stays, like the Conrad or Waldorf-Astoria

- Ink Business Preferred Credit Card for stays at Ritz-Carlton or St. Regis

But some of us aren’t so interested in top-tier hotels and instead prefer more modest accommodations. Maybe you like to go on road trips to locations where you can’t find more upscale chains like Hyatt or Marriott/Starwood, or frequently travel for work to smaller cities and towns where there aren’t big name-brand hotels. But you can find inexpensive chains like Best Western, Choice Hotels, and Wyndham just about anywhere.

If you’re a fan of these chains, you might have considered applying for one of their credit cards. But the best hotel credit cards for budget chains might not be so obvious!

I’ll show you why hotel cards for Best Western, Choice Hotels, and Wyndham aren’t always your best bet if you like staying at these brands.

What’s the Best Hotel Credit Card for Budget Hotel Chains?

If you like Choice Hotels, Best Western, or Wyndham, you’re not alone. It’s easy to find them in even the most off-the-beaten-path locations, and they’re often family-friendly with perks like free breakfast, indoor pools, and on-site laundry. Plus, they’re usually less expensive than major chains like Hyatt and Hilton.

I’ve personally had decent experiences with these brands, though mostly not for vacation or fun. They’re a good, cheap pick in a pinch if you’re on the road and need a quick spot to stay, have to work in a remote location, or need to travel for a family emergency or last-minute trip.

Choice Hotels include brands like Comfort Inn, Quality Inn, Sleep Inn, and Rodeway Inn. Best Western subdivides their hotels into brands like Best Western Plus and Best Western Premier. And you’ve no doubt seen many Wyndham hotels along the interstate, like Days Inn, Super 8, Microtel, and Travelodge.

You might think you don’t have a lot of options to earn credit cards rewards for free stays at these brands. And, to be honest, sometimes these hotels are so inexpensive you’re better off paying cash than wasting points.

Each of these chains does have their own credit card, but I’ll show you why these aren’t the best pick for most folks in a second.

- Best Western: The Best Western Rewards MasterCard, issued by First Bank, earns up to 70,000 Best Western points after meeting tiered minimum spending requirements: Earn 50,000 points after you spend $1,000 on purchases in the first 3 billing cycles, and 20,000 points when you spend at least $5,000 on purchases during each 12 billing cycle period. Best Western says their hotels cost on average 16,000 points per night.

- Choice Hotels: The Choice Privileges® Visa Signature® Card, issued by Barclays, earns 32,000 Choice points after spending $1,000 on purchases in the first 90 days of opening your account. Choice Hotels award nights start at 6,000 points, but usually cost more – up to 30,000+ points in some locations.

- Wyndham: Barclays offers 2 versions of the Wyndham Rewards® Visa® Card. The no-annual-fee card comes with 15,000 Wyndham points after your first purchase. And the annual-fee ($75) version offers 15,000 Wyndham points after your first purchase, and an additional 15,000 Wyndham points after you spend $1,000 on purchases within the first 90 days of account opening. Award nights at any Wyndham hotel cost 15,000 points per night.

None of these welcome bonuses are particularly exciting unless you really like these chains and have already gotten more valuable cards from Chase, AMEX, Citi, and the like. And for regular spending, their earnings are the pits. I’d honestly only recommend these cards if you have frequent paid stays at these hotel chains, because you’ll earn bonus points as follows:

- Best Western Rewards MasterCard – Earn an extra 10 Best Western points per $1 (20 total including what you’ll get for being a member) on Best Western Stays. All other purchases earn 2 Best Western points per $1.

- Choice Privileges Visa Signature Card – Earn an extra 5 Choice points per $1 (15 total including what you’ll get for being a member) on Choice Hotels stays. And 2 Choice points per $1 on all other purchases.

- Wyndham Rewards Visa – Earn an extra 3 Wyndham points per $1 (no annual fee) or 5 Wyndham points per $1 (annual fee) on Wyndham stays. And earn 2 points per $1 on eligible gas, utility, and grocery store purchases, and 1 point per $1 everywhere else (for both cards).

If you don’t have paid stays at these brands, it makes little sense to have their cards for everyday spending. That’s because you can get much more value from your dollar with flexible points programs like Chase Ultimate Rewards, Citi ThankYou, and Capital One Venture miles, and still redeem those points for stays at these hotels.

Don’t Lock Yourself Into Any of These Hotel Programs

I’m going to use Choice Hotels as an example because they’re an AMEX Membership Rewards transfer partner (the other 2 chains aren’t partners with any major flexible points program). And (shameless admission) because I actually have the Choice Privileges Visa Signature Card and have kept it for years because it has no annual fee. It helps increase the average age of my accounts and I throw a random small charge on it here and there to keep it active. But would I apply for it again now? Nope!

I applied for the Choice card back when I was new to miles and points (well before the Chase 5/24 rule came into effect, and I didn’t know any better). In my previous career, I spent 4 to 6 nights per month at a Comfort Inn on a corporate rate I had to pay out of pocket, so I figured earning an additional 5 Choice points per $1 spent with the card on my stays was worth it.

But Choice points are far, far less valuable than flexible points like Chase Ultimate Rewards or Citi ThankYou points. And now, if I stay at Choice (or Best Western, or Wyndham), I’ll pay with cards like my:

- Ink Business Preferred: I use this when traveling for work – it earns 3X Chase Ultimate Rewards points per $1 on travel (including hotels)

- Citi Premier Card: This personal card earns 3X Citi ThankYou points per $1 on travel (including hotels)

Collecting Chase Ultimate Rewards or Citi ThankYou points makes more sense, because they’re flexible and don’t lock you into a single hotel or airline program. And you can redeem them for stays at just about any hotel chain (and non-chain hotels, too – here’s Keith’s post about using Chase Ultimate Rewards points for stays at boutique hotels).

Or for even more simplicity, consider a card like the Capital One® Venture® Rewards Credit Card. You can redeem Venture miles at a rate of 1 cent each for paid travel, including hotels. Just purchase your stay with the card, and you’ll have 90 days to “erase” the charge with your miles.

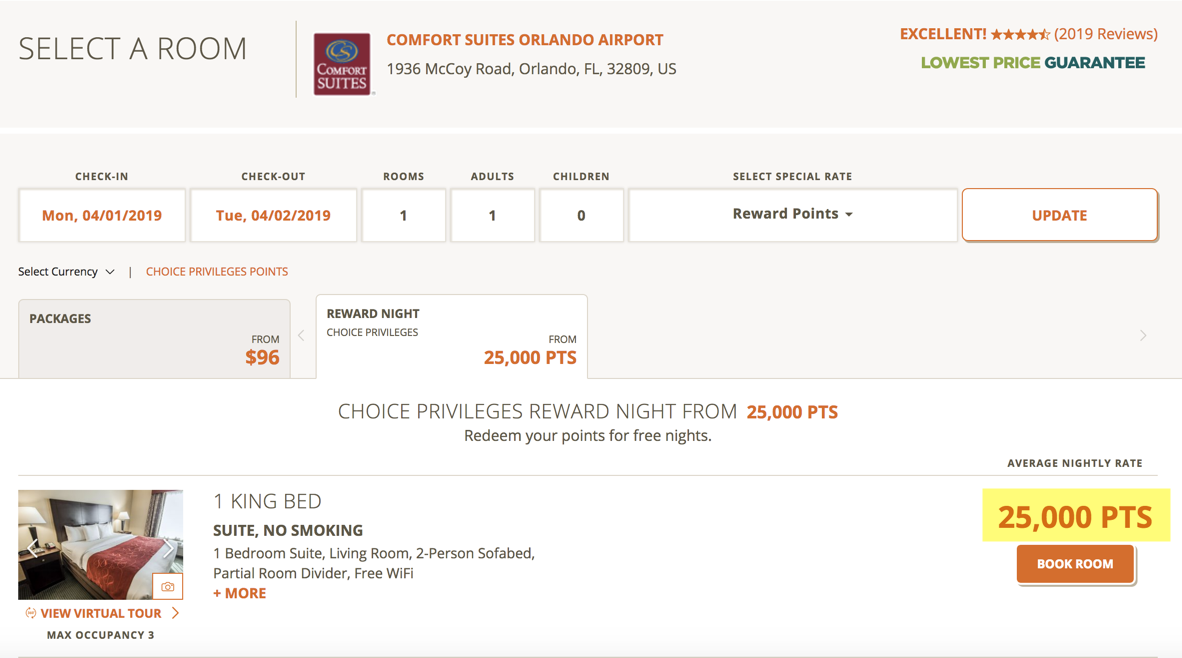

Here’s an example: The Comfort Suites Orlando airport costs 25,000 Choice points per night. That’s a lot for a Choice hotel.

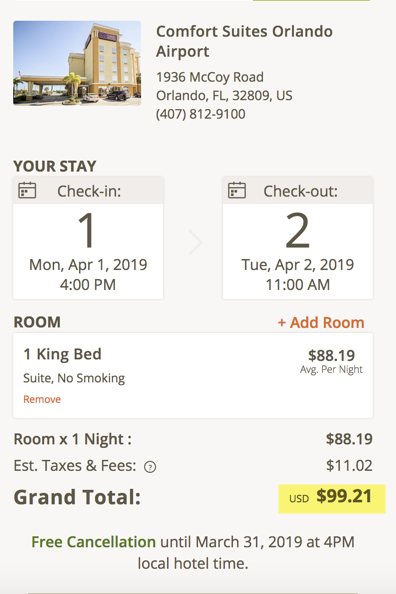

If you paid cash, you’d be out of pocket ~$99 including taxes. So in this case, you’d be getting a dismal ~0.4 cents per point (~$99 rate / 25,000 points).

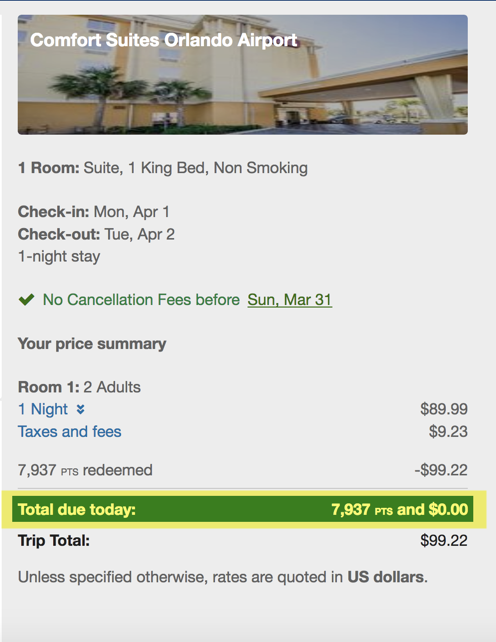

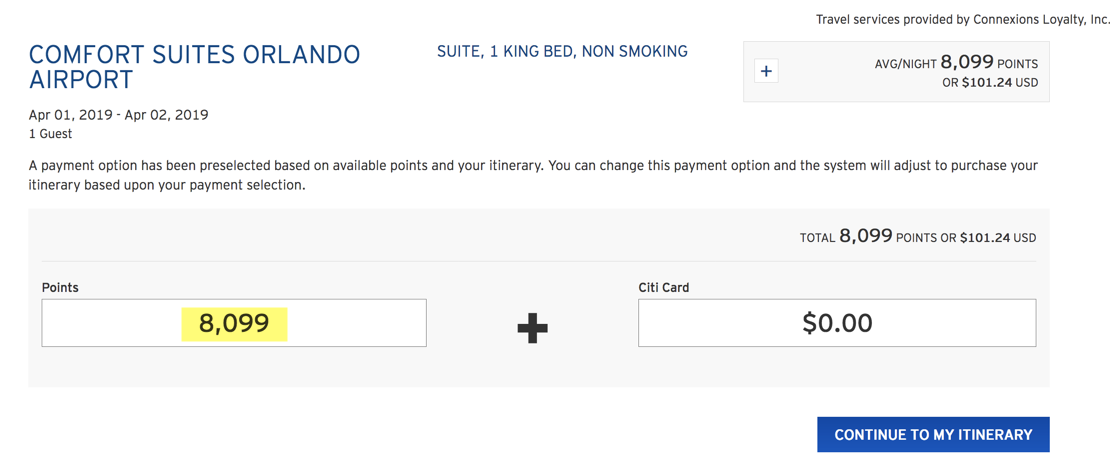

However, you can find the exact same hotel at a similar rate through the Chase Ultimate Rewards travel portal. And redeem Chase Ultimate Rewards points (or cash, or a combination of points and cash) for the stay. In this case, because I have the Chase Sapphire Preferred Card and Ink Business Preferred, my Chase Ultimate Rewards points are worth 1.25 cents each.

You’d pay even fewer points if you have the Chase Sapphire Reserve, because with that card your Chase Ultimate Rewards points are worth 1.5 cents each. So in this case, you’d only have to spend 6,615 Chase Ultimate Rewards points (~$99 rate / 1.5 cents per point).

Similarly, if you have the Citi Premier, your Citi ThankYou points are worth 1.25 cents each when you book through the Citi ThankYou travel portal. In this example the rate is a couple of dollars higher so you’ll pay slightly more points.

Now, I’m not suggesting that Choice points and Chase Ultimate Rewards points have equal values – far from it. Chase Ultimate Rewards points are much more valuable than Choice points. And most folks are able to squeeze more than 1.25 to 1.5 cents per Chase Ultimate Rewards point by transferring them to airline and hotel partners instead of booking through the portal.

Let’s have a look at what you’d have to spend in non-bonus categories to earn enough points for the stay above with the Choice Hotels card versus the Chase Sapphire Preferred / Citi Premier, Chase Sapphire Reserve, or Capital One Venture. I’ll round up to a $100 room rate for simplicity.

- The Choice Privileges® Visa Signature® Card – $12,500 to earn 25,000 Choice points (25,000 points / 2 Choice points per $1 for unbonused spending)

- Chase Sapphire Preferred / Citi Premier – $8,000 to earn 8,000 Chase Ultimate Rewards or Citi ThankYou points (8,000 points / 1 point per $1 for unbonused spending)

- Chase Sapphire Reserve – ~$6,667 to earn 6,667 Chase Ultimate Rewards points (6,667 points / 1 point per $1 for unbonused spending)

- Capital One Venture – $5,000 to earn 10,000 Venture miles (10,000 miles / 2 miles per $1 for all spending)

And you’d have to spend even less on the Chase or Citi cards if your purchases are in bonus categories like travel and dining.

Now, if the Choice points rate were lower, the numbers would skew more in favor of the Choice Privileges Visa. And personally, I’d never redeem Chase Ultimate Rewards or Citi ThankYou points for a stay like this, because I prefer transferring them to airline and hotel partners – I’d just pay cash instead.

But if getting free stays at Choice Hotels or other budget chains is your travel goal, this strategy can make a lot more sense than collecting Choice points from their credit card.

Note: I mentioned Choice is an AMEX Membership Rewards transfer partner. It rarely makes sense to transfer AMEX points to Choice because you can get much more value redeeming them in other ways. Here’s more about when it makes sense to transfer AMEX Membership Rewards points to hotel partners.

You can apply similar math to booking Best Western or Wyndham hotels. Although Wyndham is a little different, because any of their hotels cost 15,000 Wyndham points per night – from the most downscale Travelodge to high-end Wyndham Grand Resorts. It can make more sense to collect Wyndham points if you’ll redeem them for otherwise expensive stays.

Bottom Line

If you prefer budget hotels like Best Western, Choice Hotels, or Wyndham, you may have considered applying for one of their credit cards. This really only makes sense if you’re a huge fan or have a lot of paid stays at these brands.

While you’ll earn bonus points for paid stays at these chains, these cards are rarely a good idea for day-to-day spending. The best hotel credit cards for budget chains don’t have the hotel name attached to them!

You can get far bigger bang for your buck if you collect flexible points and miles like from cards like:

- Chase Sapphire Preferred Card

- Ink Business Preferred

- Chase Sapphire Reserve

- Citi Premier Card

- Capital One Venture Rewards Credit Card

You can redeem Chase or Citi points through their travel portals for free stays at nearly any hotel, including budget brands and boutique hotels. No need to collect specific hotel points, and you’re not locked into a single hotel or airline program because these points are flexible. And you can use Venture miles to erase just about any travel purchase when you pay with your card.

As always, consider your travel goals before pulling the trigger on any credit card. And remember, if you’re new to miles and points, we always recommend applying for Chase cards first because of their 5/24 rule.

Do you redeem points to stay at chains like Best Western, Choice Hotels, or Wyndham? What’s your strategy?

Editorial Note: We're the Million Mile Secrets team. And we're proud of our content, opinions and analysis, and of our reader's comments. These haven’t been reviewed, approved or endorsed by any of the airlines, hotels, or credit card issuers which we often write about. And that’s just how we like it! :)

Join the Discussion!