That’s It, I’m Done With Airline Miles and All-In on Flexible Rewards (Think Chase Ultimate Rewards Points)

Signing up for credit cards through partner links earns us a commission. Terms apply to the offers listed on this page. Here’s our full advertising policy: How we make money.

Update: One or more card offers in this post are no longer available. Check our Hot Deals for the latest offers.

INSIDER SECRET: With Chase Ultimate Rewards points, you have the option to transfer your points to Ultimate Rewards points transfer partners including United Airlines, Singapore Airlines, Hyatt, and more. That gives you far more options than earning miles from a single loyalty program.

My travel rewards strategy is primarily driven by my spending habits and travel goals, but it’s always evolving. After United Airlines announced it is ditching its award chart, I’ve come to the conclusion that earning airlines miles is just too limiting.

Sure, there are always devaluations, but this was the last straw for me. The fact is, a majority of the best credit cards for travel earn flexible rewards, not airline- or hotel-specific rewards. While focusing on earning just one type of miles or points might make sense for some, I’d be willing to bet that flexible rewards points are the way to go for most.

Here’s a quick example.

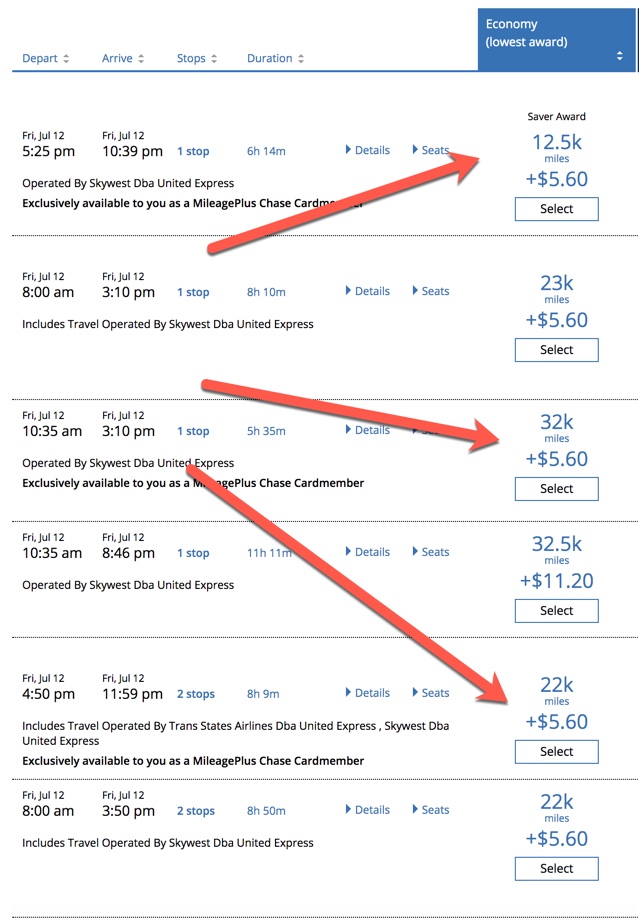

I fly between Missoula and Santa Barabara a handful of times each year to visit my sister, and I’ve never had much of an issue finding award seats for 12,500 United Airlines miles. But recently, I’ve seen an increase in award prices and fewer saver awards available, even as a United℠ Business Card cardholder who has access to more award seats.

As you can see below, there’s one flight pricing out at 12,500 miles and the rest range anywhere from 22,000 miles up to 32,500 miles.

That’s not even accounting for the fact that United Airlines charges a close-in booking fee for award tickets. So if you don’t book 21+ days in advance, you’ll pay an extra $75 fee for booking a ticket with miles.

So what are the alternatives?

My defense against more airlines (and hotels, too) doing away with award charts and moving to dynamic pricing is earning flexible rewards points.

Flexibility is key, and the best way to maintain flexibility in your credit card strategy is to earn transferable rewards. My favorites are Chase Ultimate Rewards points, Amex Membership Rewards points and Capital One Venture miles.

For example, there are over a dozen AMEX airline partners to which you can transfer your AMEX Membership Rewards points, including Delta and British Airways.

These are my favorite cards for earning Amex Membership Rewards points:

- The Platinum Card® from American Express (Best Amex membership rewards card for frequent travelers)

- The Business Platinum Card® from American Express (Best Amex membership rewards card for small business owners)

I especially value the Amex Business Platinum card because you get 35% of your points back for all flights, including coach tickets, booked with your selected airline through the AMEX travel portal. Terms apply.

In comparison, with Chase Ultimate Rewards, you have the option to transfer your points to Ultimate Rewards points transfer partners including United Airlines, Singapore Airlines, Hyatt and more.

Here are my favorite cards for earning Chase Ultimate Rewards:

- Chase Sapphire Reserve (Best Ultimate Rewards credit card for frequent travelers)

- Ink Business Preferred Credit Card (Best Ultimate Rewards credit card for small business owners)

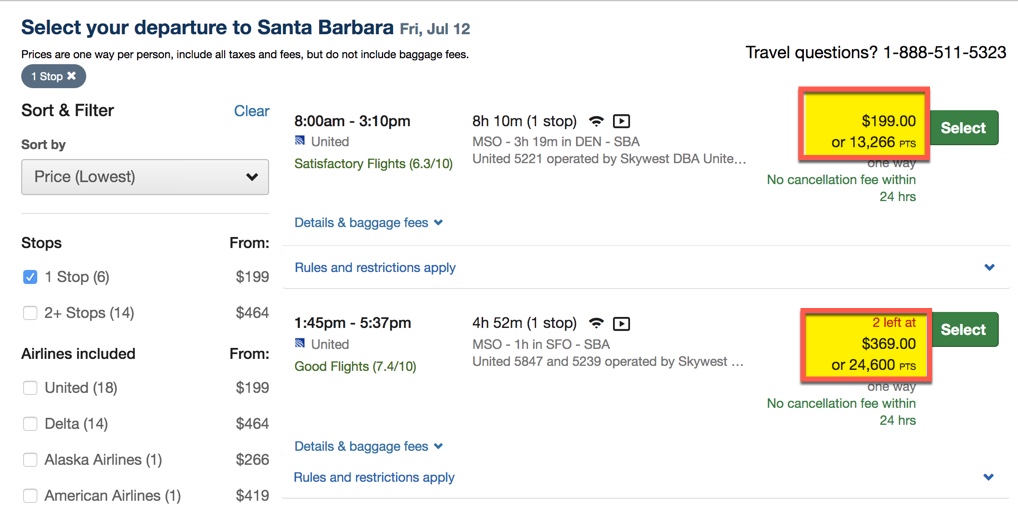

Going back to the example above, I found many of the exact same flights bookable with Ultimate Rewards points through the Chase travel portal for far fewer points.

The flight departing at 8am on July 12 cost just 13,266 Chase Ultimate Rewards points, but you’d pay 23,000 miles if you booked it through United Airlines. That’s a savings of 9,734 points one-way.

Multiply that across multiple bookings and you can see how the savings you get booking with flexible rewards versus airline miles could really add up.

Finally, you could consider earning flexible rewards like Capital One Venture miles because they’re so incredibly easy to use. The best card for earning Venture miles is:

- Capital One Venture Rewards Credit Card (Card with the easiest to redeem rewards)

Just make a qualified travel purchase with your card then use your rewards to “erase” it from your bill. There’s no searching for award seats or worrying about blackout dates.

Bottom Line

Nothing lasts forever in the world of miles and points. Airlines can adjust award charts or even do away with them altogether, so it’s best to figure out a travel rewards strategy that works for you.

I’ve personally moved away from earning miles and points on any one particular airline and started focusing my efforts on flexible rewards including:

- Chase Ultimate Rewards points

- Amex Membership Rewards points

- Capital One Venture miles

In doing so I’ve been able to save tens of thousands of miles on award tickets and avoid numerous close-in booking fees. It’s no wonder a majority of the best credit cards for travel earn flexible rewards.

For the latest tips and tricks on traveling big without spending a fortune, please subscribe to the Million Mile Secrets daily email newsletter.

Editorial Note: We're the Million Mile Secrets team. And we're proud of our content, opinions and analysis, and of our reader's comments. These haven’t been reviewed, approved or endorsed by any of the airlines, hotels, or credit card issuers which we often write about. And that’s just how we like it! :)

Join the Discussion!