How My Credit Score Went Up 95 Points After Five Years of Collecting Miles and Points

Signing up for credit cards through partner links earns us a commission. Terms apply to the offers listed on this page. Here’s our full advertising policy: How we make money.

INSIDER SECRET: Instead of canceling a credit card to avoid an annual fee, try downgrading it to a no-annual-fee card to protect the length of your credit history.

When I talk with people about my adventures traveling with credit card points, one of the first questions I get is along the lines of, “Isn’t that bad for your credit?” In fact, most people think that opening credit cards hurts your credit and that having too many credit cards can prevent you from getting loans for a house or car.

These people are usually shocked when I tell them that at any given time, I have 12-15 credit cards open (many of which are on the list of the best credit cards for travel).

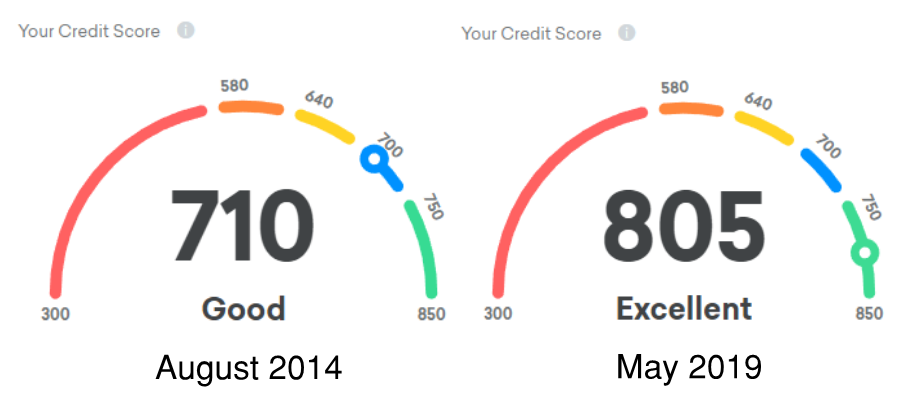

Despite what most people believe, opening credit cards to earn points is a great way to increase your credit score. My credit score has gone up by 95 points (from a fairly decent 710 to an outstanding score of 805) since getting into the world of miles and points in 2014!

How Your Credit Score Is Calculated

According to myfico.com, your FICO credit score is calculated based on the following criteria:

- Payment History: 35%

- Amounts Owed: 30%

- Length of Credit History: 15%

- Credit Mix: 10%

- New Credit: 10%

The three major credit bureaus, Experian, Equifax and Transunion, calculate their scores a little differently but they are all based on these criteria. There are also some alternate scores, like the VantageScore, which ranges from 501-990 instead of the standard 300-850 range for the FICO score.

How Credit Cards Can Help Your Score

Based on the criteria above, two factors – payment history and amounts owed – account for 65% of your credit score. Fortunately, credit cards can help with both of these.

Payment history, which accounts for 35% of your credit score, is a measure of how well you have paid your credit accounts on time. A strong record of on-time payments will increase your credit score, but missing even one payment can hurt your score.So if you have multiple credit card accounts that you pay on time every month, you should see your score increase steadily over time.

Amounts owed, which accounts for 30% of your credit score, is a measure of how much you owe on your credit accounts compared to your total available credit (also called the credit utilization ratio). According to myfico.com:Your credit utilization ratio on revolving accounts — the percentage of your available credit you’re using — is an important factor in your FICO® Scores. Using a high percentage of your available credit means you’re close to maxing out your credit cards, which can have a negative impact on your FICO Scores. On the other hand, using a low percentage of your available credit can have a positive impact.

By opening up multiple credit cards, you increase your total available credit and thus decrease your credit utilization. Maintaining a low utilization ratio over time should increase your credit score.

How My Score Went Up

Over the last five years, I have opened up 2-3 new credit cards each year. I typically wait for a good intro bonus on one of the best credit cards for travel and look for cards that I want to keep because of their perks and benefits. Each time I open a new credit card, my total amount of available credit increases, which has a positive impact on my credit score.

With all of my credit cards, I pay the entire balance in full every month, on time. This habit adds another month of clean payment history to my credit report each month, which also has a positive impact on my credit score.

While 12-15 credit cards may seem like a lot to some people, especially if those cards carry an annual fee, I review my credit card lineup each year to determine if I should keep each particular card. If I use a card frequently or if the benefits outweigh the annual fee, I keep the card in my wallet.

Key Tips for Increasing Your Credit Score Through Collecting Miles and Points

Anyone with a credit card can increase their credit score over time by following a few simple tips:

Pay off your credit cards every month

Remember that 30% of your credit score is based on the amounts owed. While opening up new credit cards decreases your credit utilization ratio (which should improve your score), a balance on your credit card increases this ratio (which may hurt your score).

Perhaps more importantly, most travel credit cards have high interest rates. The amount you pay in interest will far outweigh any points or miles you get from the card. As a general rule of thumb, if you can’t pay off a credit card balance every month, you shouldn’t use the card.

Keep your first credit card forever

Remember that your length of credit history is 15% of your credit score. Keeping accounts open for longer periods of time is viewed as a positive in the FICO calculations and should increase your score over time.

Keep cards open by downgrading to a card without an annual fee

Many people close a credit card because they don’t want to pay the annual fee. If you are thinking of closing a card, consider calling your credit card company to see if they can switch your account to a card without an annual fee. In most cases, the credit card issuer can do this for you over the phone. This strategy keeps the account open (remember 15% of your score is the length of your credit history) while taking the annual fee off your plate.

Bottom Line

Despite what many folks believe, opening up credit cards and paying them on time every month is a great way to increase your credit score. By using this simple strategy, I increased my credit score by 95 points in just under five years.

Each year, I review credit cards and keep the ones I use frequently or that offer good benefits. I downgrade or cancel a card that I don’t use anymore if I find it isn’t worth the annual fee when considering my personal travel goals. While this is a great strategy, it only works when you pay your credit cards bill in full on time. Carrying a balance on credits cards month to month, especially on a travel rewards card, will negate any bonus points that you earn.

For the latest tips and tricks on traveling big without spending a fortune, please subscribe to the Million Mile Secrets daily email newsletter.

Editorial Note: We're the Million Mile Secrets team. And we're proud of our content, opinions and analysis, and of our reader's comments. These haven’t been reviewed, approved or endorsed by any of the airlines, hotels, or credit card issuers which we often write about. And that’s just how we like it! :)

Join the Discussion!