Update: One or more card offers in this post are no longer available. Check our Hot Deals for the latest offers.

There are 171,000 words in the English dictionary, and I cannot find one that accurately expresses how fabulous card intro offers are nowadays. Free travel is super easy to achieve just by opening one single credit card.

If you’re new to miles and points, you might not appreciate the current offers we’re seeing. Just a couple years ago, the standard Chase Sapphire Preferred® Card welcome offer was 40,000 points after meeting minimum spending requirements. The current offer is DOUBLE that figure. We estimate Chase points are worth 1.7 cents on average. So while this card’s offer was once worth $680 in travel, it’s now worth more like $1,360.

Card issuers are crafting bigger and better bonuses for their travel credit cards so frequently that I actually look forward to waking up in the morning. This prompts the question: Should you scoop up some welcome bonuses now while they’re extra juicy? Or should you wait a while longer and see what other goodies present themselves in the coming months?

Travel credit cards are offering hall-of-fame bonuses

I’ll show you what I’m talking about.

My favorite increased offer, the Marriott Bonvoy Boundless™ Credit Card, comes with 5 free night certificates (worth up to 50,000 points each) after you spend $5,000 on purchases in the first three months from account opening. That’s potentially 250,000 points — we estimate Marriott points are worth 0.8 cents each, making this bonus worth potentially $2,000 in hotel stays.

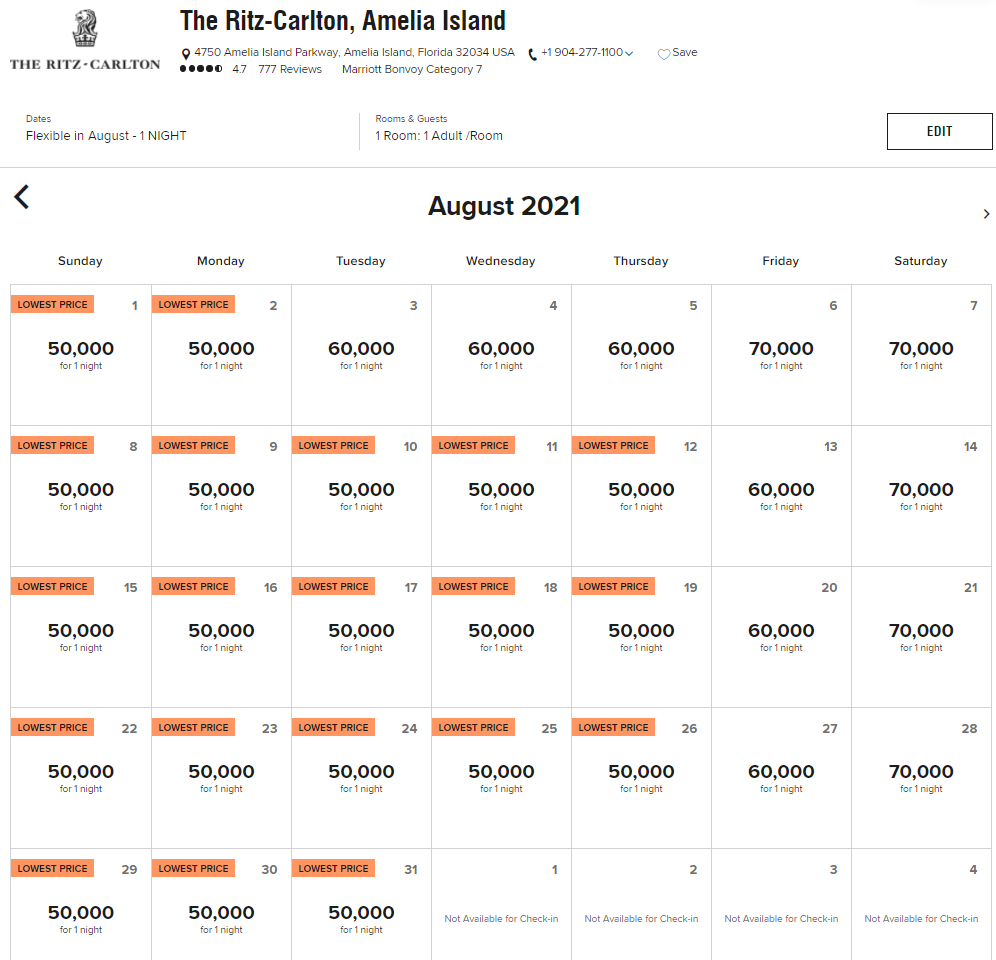

That is far more than twice the value this card’s bonus has ever offered. Previously, its best-ever bonus was 100,000 points (though note that free night certificates aren’t as versatile as points — read our Bonvoy Boundless review for more details). With this card bonus, it’s possible to get five free nights at hotels like The Ritz-Carlton, Amelia Island in Florida, which sells for 50,000 points per night on off-peak dates. That same night in cash could be $550+!

In other words, you could get $2,750 in hotel stays with this card bonus. That may be one of the greatest bonuses you will EVER see.

So should you earn a bunch of bonuses now?

Bonuses like the ones above have been cropping up in recent months. It’s indicative of things to come, as card issuers are hurting from people opening fewer credit cards and traveling less. Who knows what belle of the ball will be released tomorrow?

The answer is, earn every bonus you think you’ll use in 2021. But don’t apply for a card until the increased offer’s end-date is announced. This way, you can wait for other offers and still apply for an amazing bonus last-minute if you perceive it’s your best option.

[ Subscribe to our email newsletter for more points, miles and credit card strategies ]

Case in point, the Chase Sapphire Preferred 80,000-point bonus may not be around for much longer. We don’t know what the bonus will drop to (or exactly when, but it may be soon), but we know it won’t be nearly as generous.

If you’re eligible for the Chase Sapphire Preferred bonus (see our posts on the Chase 5/24 rule and the Chase Sapphire rules), you can wait a few weeks to apply, just in case a better card bonus presents itself. For example, the Chase Sapphire Reserve® once offered 100,000 points after meeting minimum spending requirements (currently offering 50,000 bonus points after spending $4,000 in the first three months). It’s not outrageous to see something like that happen again in this climate of card issuers hyper-driven to acquire new customers.

The golden rule

Just a couple of weeks ago I got burned, BADLY. I had been eyeing the Marriott Bonvoy Business™ American Express® Card for a few months. I got impatient and opened the card with a bonus of 75,000 points after meeting minimum spending requirements. Solid bonus, right?

A month after I was approved, the card now offers:

- 100,000 points after you spend $5,000 in purchases within your first three months of account opening

- Up to $150 in statement credits within your first six months of card membership for all eligible purchases on U.S. Advertising in select Media

- Complimentary Marriott Bonvoy Platinum Elite status for one year (Feb. 1, 2021 – Jan. 31, 2022)

- Offers end Jan. 13, 2021

- $125 annual fee (see rates & fees)

- Terms Apply

That is great news for you, but devastating news for me.

The golden rule is this: Don’t apply for any credit card unless its welcome bonus is higher than usual. You can bookmark our BonusTracker page to keep up to date on all the improved offers as they are released. A simple strategy is to strictly apply for the cards on that page.

We REALLY appreciate when you apply for cards through our links, since they help us keep the lights on. However, it’s important to us that you’re always getting the biggest, fattest bonus — so if there’s a card you’d like to open, check the BonusTracker page to see if it’s on there. If you can stall your application for a month or two, do it. Additionally, referral offers can sometimes be higher than public offers, so make sure to check around for any better deals.

Bottom line

If you have an immediate need for a certain card, you should obviously open it. But heed the advice of someone who pulled the trigger too early on a recent credit card: Lack of patience can cause you to miss out on tens of thousands of points per card bonus, equaling hundreds of dollars in loss.

Check our Credit Card BonusTracker page for all the exceptionally high bonuses incited by credit card issuers pleading with you to give their cards a try. By the time you’re ready to travel, you’ll have a stockpile of rewards to fund your adventures for a long time.

Subscribe to our newsletter for more credit card advice and tips delivered to your inbox once per day.

For rates and fees of the Marriott Bonvoy Business card, click here.