Update: One or more card offers in this post are no longer available. Check our Hot Deals for the latest offers.

We talk almost exclusively about airline miles and hotel points at MMS. Award charts, peak and off peak pricing, transfer partners, etc. are our favorite ways to travel for free. However, if you’re not into all that complicated stuff, you can use credit cards to earn another currency with which you’re much more familiar — CASH.

The best cash back credit cards can earn you hundreds (even thousands) of dollars per year if you use them for your daily spending. And nothing is easier to redeem than cash. I’ll explain exactly how cash-back cards work, and who should consider them over miles and points.

How does cash back work?

Cash back is the easiest credit card currency to redeem. Each time you swipe your card, you’ll earn a predetermined percentage back for your purchase. Some cards offer an instant rebate for your purchase, but most cards will deposit your cash rewards into a bank to be redeemed as a statement credit at your convenience. Either way, every swipe effectively discounts your purchase.

Many banks will also allow you to cash out your rewards as a mailed check or direct deposit into your checking account. Some will offer you the option of redeeming your cash for gift cards. This is just about the worst possible thing you could do with cash, for a couple reasons. Just note that some cards will prevent you from cashing out your rewards until you’ve accrued a certain balance ($25, for example).

First, cash is infinitely better than a gift card. If you simply redeem your rewards for cash, you can still use them at Chili’s and Olive Garden if you so choose — but if you change your mind, you’re not then limited to your merchant of choice. Second (and more importantly) gift cards don’t earn cash back! When you swipe that gift card, you earn nothing back. You should instead redeem your rewards for cash, swipe your card, and pay off that balance with your cash back.

Types of cash back credit cards

There are many different kinds of earning rates among cash back cards.

Some cards earn a flat rate of cash back for all purchases. For example, the Capital One® Quicksilver® Cash Rewards Credit Card earns unlimited 1.5% cash back on every purchase. That’s great for anyone who wants the simplest method of earning rewards while ensuring a decent return on all purchases. However, many of the best cash-back credit cards offer bonus categories for certain spending.

For example, the Blue Cash Preferred® Card from American Express comes with the following bonuses:

- 6% at U.S. supermarkets (up to $6,000 in purchases per calendar year, then 1% cash back)

- 6% on select U.S. streaming services

- 3% at U.S. gas stations and on transit

- 1% on other purchases

- Terms Apply

Cash back is received in the form of Reward Dollars that can be redeemed for statement credits.

Other cards offer rotating bonus categories that reward specific spending habits. The Chase Freedom® is perhaps the most popular among these cards. You’ll earn 5% cash back (5 Chase Ultimate Rewards points per dollar) on up to $1,500 in combined purchases in rotating quarterly categories (activation required) such as:

- Amazon

- Gas stations

- Supermarkets

- Select streaming services

You can check out the Chase Freedom 5% cash back calendar to see which purchases will currently receive a bonus.

Additionally, cards like the Chase Freedom, Ink Business Cash® Credit Card and Citi® Double Cash Card offer the ability to transfer your cash back to airline or hotel partners if you have certain other premium cards. You can read our posts on Chase transfer partners as an example.

The information for the Citi Double Cash Card has been collected independently by Million Mile Secrets. The card details on this page have not been reviewed or provided by the card issuer.

Cash back vs. points/miles

There is truly only a single reason to be collecting miles and points over cash back:

- Cash back is worth exactly the same, always. If you collect $30 in cash back, you can buy $30 worth of goods

- Miles and points (usually) do not have a set value. If you earn one American Airlines mile, you may receive 0.5 cents in value from it — or you might receive 12 cents in value. It all depends on how you use it

Collecting miles and points has a gigantic upside that cash back doesn’t. However, they’re not nearly as versatile as cash, and they’ve also got no guaranteed value. Let’s look at a quick example.

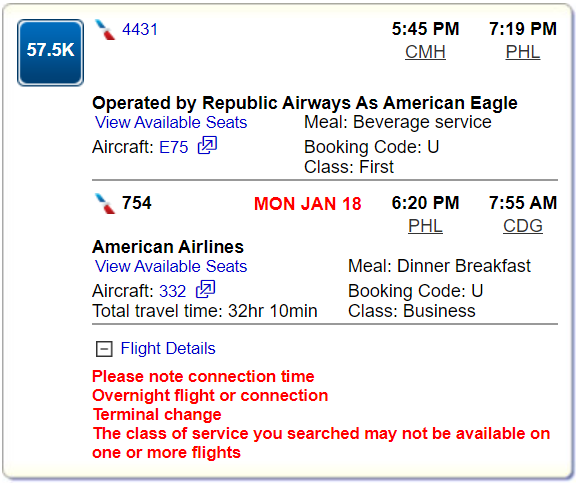

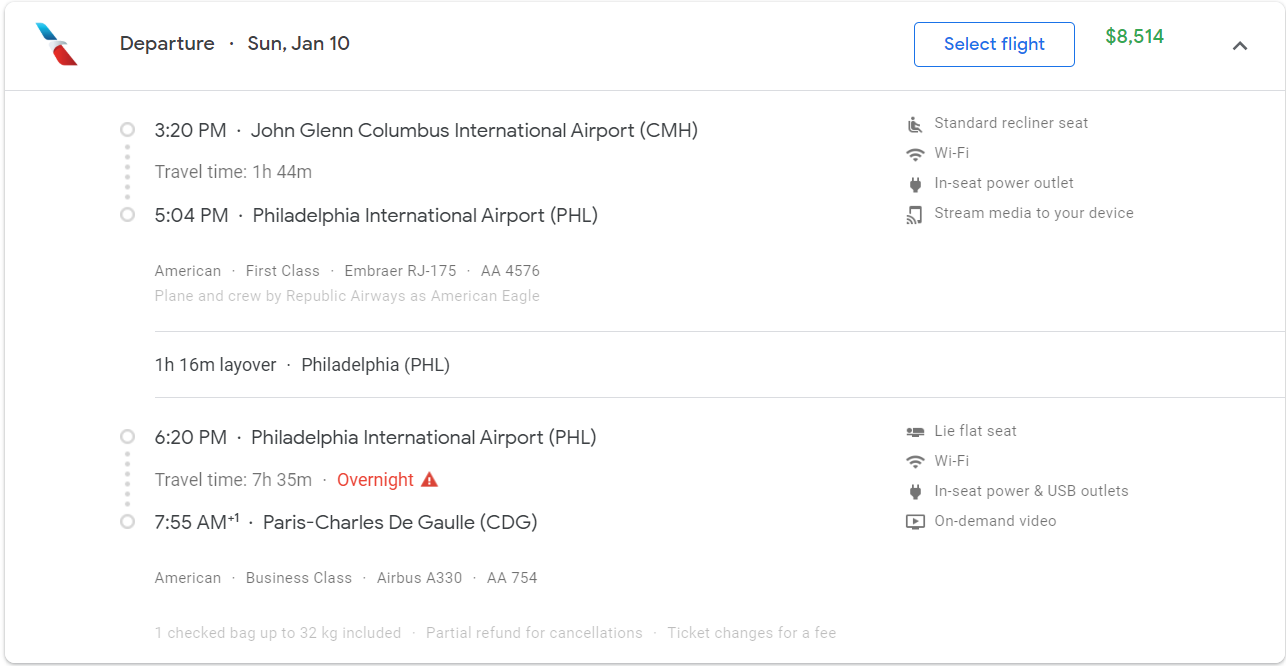

As you can see, you can reserve a flight from the U.S. to Paris in fancy business class for just 57,500 American Airlines miles one-way.

This exact same seat will cost you $8,514 if you were to purchase it from the American Airlines website. That gives you an effective value of more than 14 cents in value!

To reserve a $3,000 business class flight, you’d need to collect $3,000 on your cash back card. That means you would have to spend drastically more on your card than if you were using one of the best American Airlines credit cards like the Citi® / AAdvantage® Platinum Select® World Elite Mastercard®. The information for the Citi AAdvantage Platinum Select card has been collected independently by Million Mile Secrets. The card details on this page have not been reviewed or provided by the card issuer.

Credit cards that offer cash back

Even hardcore miles and points enthusiasts have a few cash back credit cards in their wallet. Miles and points can’t offset EVERYTHING along your travels. It’s good to have a stash of cash back cards to negate the food, gas, tolls and other random expenses you’ll encounter along your travels.

We’ve compiled a list of the best cash-back credit cards along with their best features to help you decide which cards fit your lifestyle.

| Cash back credit cards | Bonus offer | Cash back rate |

|---|---|---|

| Citi® Double Cash Card | No intro bonus | - 2% back: 1% back on all purchases and an additional 1% back when you pay off the purchases |

| Chase Freedom | $200 bonus (20,000 Chase Ultimate Rewards points) after you spend $500 on purchases within the first three months of account opening | 5% on up to $1,500 in combined purchases in rotating quarterly categories (activation required) |

| Chase Freedom Unlimited | $200 bonus (20,000 Chase Ultimate Rewards points) after you spend $500 on purchases within the first three months of account opening | 1.5% cash back (1.5X Chase Ultimate Rewards points per $1) on purchases |

| Wells Fargo Propel American Express® card The Wells Fargo Propel card is no longer available for new applicants | 20,000 bonus points (worth $200 in cash back, travel, gift cards or other rewards) after you spend $1,000 in purchases within the first three months of card opening | - 3x points on travel purchases (flights, hotels, homestays, and car rentals) - 3x points on eating out and ordering in - 3x points on gas stations, rideshares, and transit - 3x points on eligible streaming services - 1 point on all other purchases -Terms Apply |

| Capital One® Savor® Cash Rewards Credit Card | $300 cash back after you spend $3,000 on purchases within the first three months of account opening | - 4% on dining and entertainment purchases - 4% on popular streaming services - 3% at grocery stores (excluding superstores like Walmart and Target) - 1% on all other purchases |

| Blue Cash Preferred® Card from American Express | Earn 20% back on Amazon.com purchases on the card within the first six months of card membership, up to $200 back. Plus, earn $150 back after you spend $3,000 in purchases on the card within the first 6 months of card membership. Cash back received in the form of statement credits. Terms apply. | - 6% at U.S. supermarkets (up to $6,000 in purchases per calendar year, then 1% cash back) - 6% on select U.S. streaming services - 3% at U.S. gas stations and on transit - 1% on everything else - Terms Apply |

| Ink Business Cash Credit Card | $750 bonus cash back after you spend $7,500 on purchases in the first 3 months from account opening. | - 5% back (5x Chase Ultimate Rewards points per $1) on the first $25,000 you spend in combined purchases at office supply stores and on phone, internet, and cable TV services each account anniversary year - 2% back (2x Chase Ultimate Rewards points per $1) on the first $25,000 spent in combined purchases at gas stations and restaurants each account anniversary year |

Some of these cards come with monster welcome bonuses to help you travel goals (or any goals, really!). But we recommend using cards like the Ink Business Unlimited® Credit Card, Chase Freedom® and Ink Business Cash® Credit Card. They collect cash back, but give you the option to be used as travel points if you have certain other cards. For more details, read our full Chase Ultimate Rewards review.

Bottom line

Cash back is easy to collect and easy to redeem. Its greatest strength is also its greatest weakness — the flexibility that comes with earning legal tender means you can’t earn outsized value for your stash the way you can with airline miles or hotel points.

If you don’t want the hassle of worrying about blackout dates, available award seats and reward nights, changing hotel categories, or airline award charts, you’re better off collecting cash. But if you’re willing to dive into the world of award travel, subscribe to our newsletter, invest some time on MMS, and prepare to circumnavigate the world in lie-flat airplane seats.