Update: One or more card offers in this post are no longer available. Check our Hot Deals for the latest offers.

Whenever you’ve got a bunch of spending on the horizon, it’s a good time to open a travel credit card or two.

I opened the Marriott Bonvoy Business™ American Express® Card about eight days before an extended trip spanning September and October. The bonus was then 75,000 points after spending $3,000 in three months (it’s now 100,000 points after spending $5,000 in three months of account opening — plus Marriott Platinum elite status for a year. Offer ends 01/13/2021).

I had planned to exclusively use this card during my travels, to knock out the majority of that $3,000 spending requirement. The problem: It didn’t arrive in the mail before my trip! I’ve now got a little over a month to meet the full spending requirement, or I’ll miss out on 75,000 Marriott points — worth $2,172 for my upcoming travels.

Credit card welcome bonuses are the fastest way to earn free travel

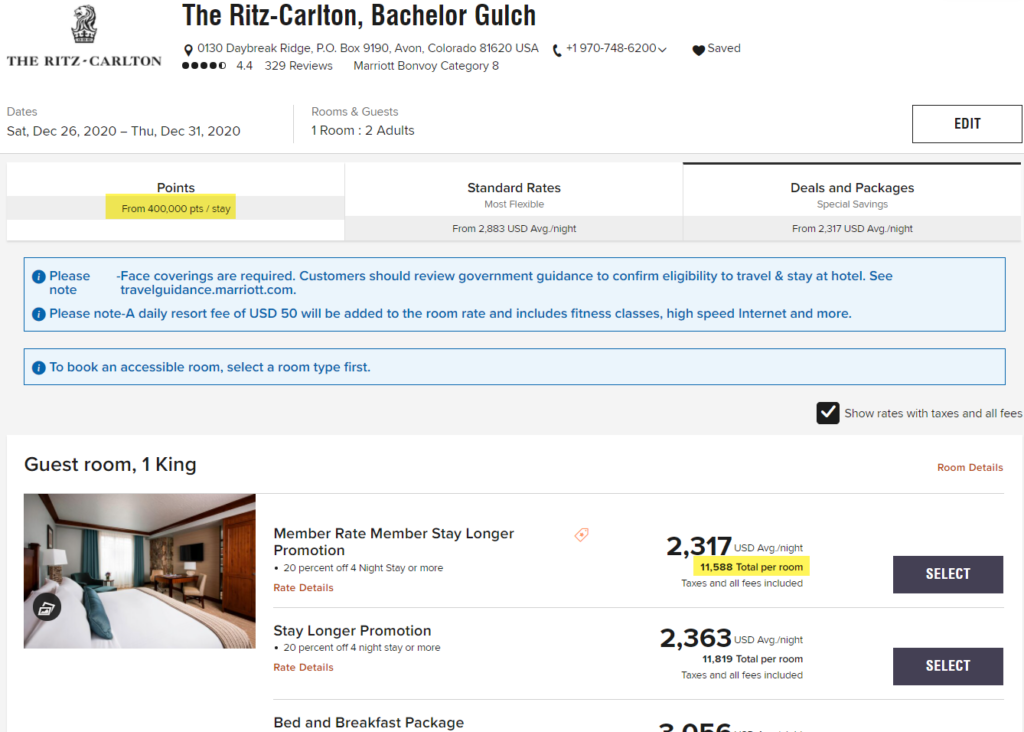

I booked a five-night award stay at the Ritz-Carlton Bachelor Gulch in Colorado on Christmas week. This is the most absurdly expensive time of year for a ski trip, with rooms costing $2,317 per night. The cash price of this stay totals $11,588!

My reservation, however, costs 400,000 Marriott points. That’s so many points — but relative to the cash price, it’s a steal. I’m getting a value of ~2.9 cents per point (a full 2.1 cents higher than our estimated value of Marriott points at 0.8 cents each).

I am almost exactly 75,000 points shy of 400,000. I need the Amex Marriott Bonvoy Business welcome bonus to reach my goal. And because I’m getting 2.9 cents in value per point for my upcoming stay, 75,000 points is worth $2,175 to me.

How to quickly meet minimum spending requirements in a bind

These are emergency ways to meet minimum spending if there’s simply no other way. Normally, just using your new card for all your spending should be enough to earn any reasonably attainable bonus. But desperate times call for the below measures.

Venmo

Venmo is a platform that allows you to transfer money from person to person with your credit card, debit card or bank account. When I add my card, I can send money to a friend or family member, and it counts as a purchase. For example, if I send $300, it’s just like I swiped my card for $300 at a store.

Venmo is totally safe to use, and pretty dummy-proof if you’re sending money to someone you trust. For example, I once accidentally sent $1,050 to my wife instead of $105. She just wrote me a check for the difference, so no harm done.

The catch? Venmo charges 3% in fees. That’s over $30 in fees to Venmo. This method is a horrendous way to earn points on your credit card, as the fees will negate any rewards you get for your spending. However, if you’re trying to meet a minimum spend requirement, it can be worth it.

Note that some banks are starting to code Venmo transfers as cash advances, so make sure you check with your bank how they treat using a credit card with venmo. Doctor of Credit has a resource on what does and doesn’t code as a cash advance.

Plastiq

Plastiq is a service that gives you the power to pay bills with a credit card that you normally couldn’t. Even if your biller doesn’t accept credit cards as payment! Examples include mortgage, rent, car payment, etc. Plastiq charges your card, and then sends a check, direct deposit or ACH transfer to pretty much anyone — even individuals.

This is a huge help for me. My apartment complex takes credit card, but they don’t take American Express — but Plastiq does. If I pay my upcoming rent payment with my card via Plastiq, that’ll be more than a third of my spending complete.

Plastiq’s catch is similar to Venmo. You’ll be charged a 2.85% fee when you transfer money from your credit card. An awful strategy to earning points, unless you’ve got an impending minimum spending requirement.

Prepare for Black Friday and Cyber Monday

I’m on the hunt for two ultrawide curved monitors for work, and I’ve been anxiously waiting since Cyber Monday of last year when I missed some really good deals.

By the time Cyber Monday rolls around, the window to meet my minimum spend will be over. Because of this, I’ll probably buy a $500 Amazon gift card now (or something similar), and spend them on Cyber Monday. That way, the spending will count toward earning my welcome bonus.

I may also purchase gas or grocery gift cards to use in the coming months.

Bottom line

If you need tips on meeting credit card spending, check out our post on 40 ways to meet a credit card’s minimum spending requirement. No matter how insurmountable a spending requirement seems, there’s almost always a way to achieve it. You can use a credit card for many more expenses than you might think.

Let us know if you have any questions! And subscribe to our newsletter for more credit card tips delivered to your inbox once per day.