Don’t forget to follow me on Facebook or Twitter!

Readers frequently email to ask about the impact of being an authorized user on someone’s credit card. There are several benefits and drawback to being an authorized user so let’s have a look!

Authorized VS. Joint Users

An authorized user is someone who can run up charges on a credit card on your behalf. An authorized user is usually not personally liable for the charges on the credit card, but the primary card holder is liable for those charges. So only add someone whom you trust as an authorized user.

You can usually add an authorized user by calling the customer service number at the back of your credit card. Some banks will let you add an authorized user online or when you apply for the card.

On the other hand, a Joint User is equally liable for the charges on the credit card. And a Joint User usually CANNOT get the credit card sign-up bonus for him or herself again (unlike an authorized user who can get the bonus separately).

Advantages of having an Authorized User

1. Help Complete Minimum Spending

Having your partner as an authorized user on a credit card accounts means that any spending on the card counts towards your minimum spending requirements and that you get the miles and points earned for the authorized user’s spending.

Because two are better than one: an authorized user can help the cardholder reach minimum spends faster.

For example, if Emily has me as an authorized user on her Chase Sapphire Preferred card, she will earn the points for the spending which I do. So we don’t need to switch the Chase Sapphire Preferred card between us.

2. Can Get Sign-Up Bonus on Your Own Later On

An authorized user won’t get the sign-up bonus for being an authorized user on someone else’s card because only the primary cardholder gets the sign-up bonus and the miles or points for spending.

But the authorized user can apply for the card in his or her own name, later on, as the primary cardholder and get the sign-up bonus. In this way both you and your partner can get a credit card sign-up bonus.

For example, I won’t get the sign-up bonus for being an authorized user on Emily’s Chase Sapphire Preferred (only she will). But I can apply for the Chase Sapphire Preferred and get the sign-up bonus myself!

3. Potentially Improves Authorized User’s Credit

If the person who adds you as an authorized user has good credit, your credit score may get a boost. This is especially true for partners/children who don’t have long credit histories.

Usually, the credit line will appear in the authorized user’s credit report even if you don’t give the bank your social security number or other personal information. But there isn’t a credit inquiry on the authorized user’s credit report.

If you’re a student or stay-at-home mom, with no income and credit history, being an authorized user will usually help establish your credit history and could improve your credit score, provided the primary card holder has good credit.

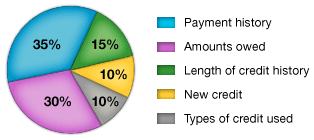

The payment history for the card will be reported on your credit report.

4. Additional Bonuses

In the past, banks would offer bonus miles when an authorized user was added to the account.

They have since scaled back and one of the few credit cards to offer such a bonus are the Bank of America Virgin Atlantic card & United Explorer cards.

Disadvantages of having an Authorized User

1. Liable for Authorized User’s Spending

The primary cardholder is responsible for all the charges of the authorized cardholder. So make sure you only add folks whom you trust as authorized users!

2. Spending Close to Credit Limits

Your credit score drops a lot as you approach the credit limit on your credit card. Having an authorized user who spends on the same credit card makes it easier to approach your credit limit. Some banks will let you set a limit to what the authorized user can spend on the card.

I try to keep the overall balance on any credit card less than 30% of the credit line. I sometimes do exceed 30%, but I then pay off the balance online the next day.

3. Potentially Decreases Credit Score

The primary cardholder’s credit score can decrease if the authorized user maxes out the credit limit on the card or makes charges which the primary user can’t pay.

The authorized user’s credit score can be negatively impacted if the primary card holder fails to make their payments on time or maintains high balances on their account.

Bottom Line

Adding an authorized user can help you complete the minimum spending requirements. But be sure that you can trust the authorized user with the card since your credit score is at stake!