Update: One or more card offers in this post are no longer available. Check our Hot Deals for the latest offers.

With more airlines moving to dynamic pricing and more hotel programs changing their award charts, Hyatt was bound to join the party at some point. And starting in March 2020, Hyatt will implement a new award chart with peak and off-peak pricing, much like Marriott did earlier this year.

I know that sounds scary, but I promise it’s not all bad news.

The good news is that in some cases, you’ll pay fewer points for certain less-popular nights than you would have paid under the old award chart. What’s unfortunate is that it will be more difficult to squeeze the most value from your points because rates will be higher during peak dates, which is when you’d normally get the most value from an award stay.

Hyatt isn’t changing its hotel award categories — they’ll remain 1-8.

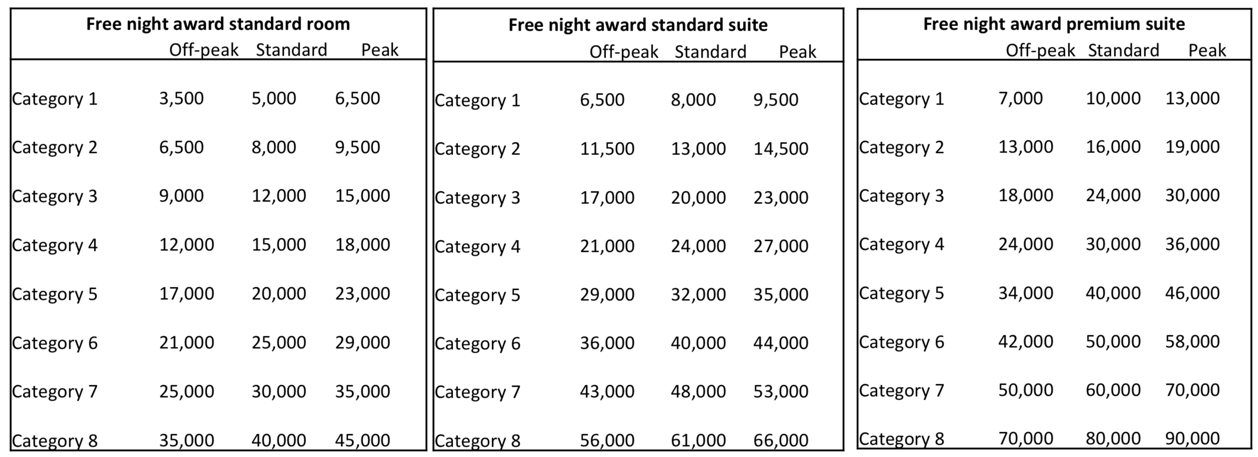

Here’s a look at the new charts:

As you can see, standard rates are staying the same. The new award chart will be applicable to all room types, from standard rooms to premium suites, and across all of Hyatt’s brands, including its all-inclusive properties and Miraval resorts. Points + Cash bookings will also move to peak and off-peak pricing, but will still require 50% off the standard cash price and 50% of the award cost for a free night.

What’s very important to note is that if you have an award booked before these changes go into effect, you’ll receive a one-time refund on the difference in points if your stay falls within the new off-peak times. Thankfully, you won’t be charged more if your existing award booking falls within the new peak pricing time frame. Hyatt also says that once peak, standard and off-peak dates are posted (usually 13 months in advance), they will not change, so you don’t need to worry about award prices changing throughout the year.

Given this, your best bet is to book any upcoming stays before these changes go into effect in March.

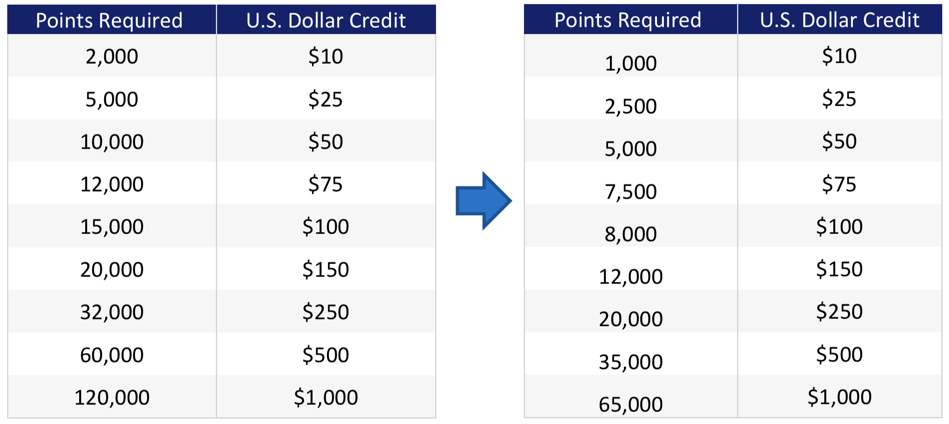

On another positive note, starting Jan. 29, 2020, you’ll get up to 50% more value from your Hyatt points when you use them for credit towards dining, spa, in-room purchases and more. For example, at the current redemption rate, you’d need to use 10,000 Hyatt points for a $50 credit. Now you’ll only need 5,000 points for a $50 credit.

Here’s a look at the old and new redemption rates:

If you use 65,000 Hyatt points for a $1,000 spa and dining credit, for example, you’ll get a value of over 1.5 cents per point, which is a decent deal.

You can find all the details of these updates to the Hyatt award chart, and more, here. And stay tuned for more analysis, once these rates go live, on how these changes will affect the value you’ll be able to get for your Hyatt points going forward.

Ways to earn Hyatt points

If you’re looking to earn more Hyatt points, consider the World of Hyatt Credit Card. With it you can earn up to 60,000 Hyatt points after you meet tiered spending requirements:

- 30,000 Bonus Points after spending $3,000 on purchases within the first 3 months from account opening.

- Plus, up to 30,000 more Bonus Points by earning 2 Bonus Points total per $1 spend on purchases that normally earn 1 Bonus Point, on up to $15,000 in the first six months of account opening.

And don’t forget, you can also transfer Chase Ultimate Rewards points to Hyatt at a 1:1 ratio, from cards like:

- Ink Business Preferred℠ Credit Card – 80,000 Chase Ultimate Rewards points after you spend $5,000 on purchases within the first three months of account opening

- Chase Sapphire Preferred® Card – 60,000 Chase Ultimate Rewards points after you spend $4,000 on purchases in the first three months of account opening

- Chase Sapphire Reserve® – 50,000 Chase Ultimate Rewards points after you spend $4,000 on purchases in the first three months from account opening

There’s no fee to convert points, and transfers are usually instant. Subscribe to our newsletter for more breaking travel news you can use.