Don’t forget to follow me on Facebook or Twitter!

Update: You can no longer load a Vanilla Visa to your Bluebird.A Million Mile Secrets reader (thanks!) pointed me to this FlyerTalk thread which discusses the new ability to add a Personal Identification Number (PIN) to a prepaid Visa or MasterCard debit gift card.

This is good news because you can NOW use your Visa or MasterCard gift card as a debit card with your PIN to:

- Load your American Express Bluebird at Wal-Mart

- Buy Money Orders at Wal-Mart, grocery stores or other locations to pay loans etc.

- Get Cash Back at certain stores

- Buy Pre-Paid cards from stores which don’t sell them with a credit card, but let you use a debit card

- Potentially pay a lower debit card fee when you pay your taxes

This means that it becomes easier to complete the minimum spending requirement on your new credit cards or to use credit cards for purchases which otherwise couldn’t be made with a credit card.

Unfortunately, you can’t use the cards to withdraw money from an ATM.

According to this article, the Federal Reserve has provided informal guidance that all Visa or MasterCard pre-paid cards or gift cards have to have PIN number from April 1, 2013.

WARNING

Not all Visa and MasterCard gift cards currently let you use a PIN, so buy a small denomination gift card first to see if it makes sense for YOU. Also, getting cash back seems to vary – in my experience – based on retailer, so my experiences may not be the same as yours.

Buying a small amount of money orders to pay your babysitter, mortgage or to pay student loans could be worth it to earn miles & points.

Buying lots of money orders just to deposit in your bank account for the miles and points will arouse suspicion – at the banks and at the places you buy them from. That’s because anyone can buy money orders and deposit them in banks and “launder” money.

If the banks get suspicious, they may file a Suspicious Activity Report to the Financial Crimes Enforcement Network. Or they may shut down your account without allowing you to explain the transactions.

In addition, most sellers of money orders will ask for identification and take down your social security number, driver’s license and other identifying information if you usually attempt to buy more than $3,000 in money orders at a time, and most will not sell you more than $10,000 worth of money orders a day. But you shouldn’t need such high limits if you use them for genuine transactions.

My Experience Using Gift Cards With a PIN

In my experience, some gift card manufacturers are scrambling to get systems in place and not all of them let me register or use a PIN with my Visa or MasterCard gift card.

But they were aware of the requirement and the customer service reps indicated that I would be able to use a PIN very soon. Note that there are different issuers of the pre-paid Visa and MasterCard and they each have a different process to register a PIN. Some make you call in to register a PIN and some make you do it online.

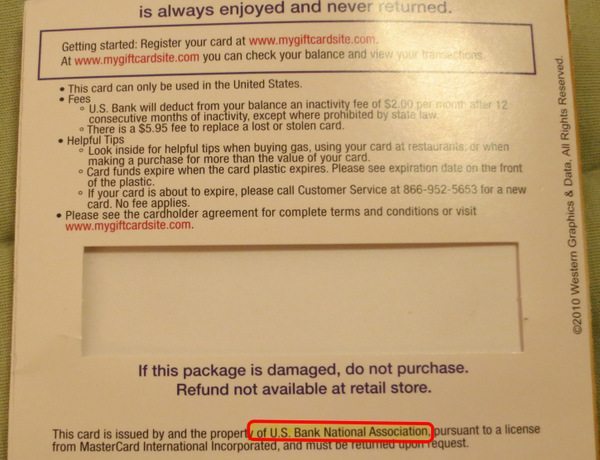

MasterCard and Visa Card Bought at Dillon’s/Kroger

I bought a $100 MasterCard & Visa gifts card from Kroger since I couldn’t find a higher denomination card and paid the $5.95 activation fee. These cards were issued by US Bank and looked like this. Unfortunately, the MasterCard version didn’t let me use a PIN, but the Visa version did!

The backs of the gift card looked liked this.

I was thrilled when I got a separate receipt which asked me to call 1-866-952-5653 to select a PIN. It also mentioned that I couldn’t use the card to withdraw cash from an ATM.

I called 1-866-952-5653 and pressed: option 1 for “English“, then option 2 for “other inquiries” then option 3 for “Setting a PIN.” I entered a 4 digit PIN and confirmed the number.

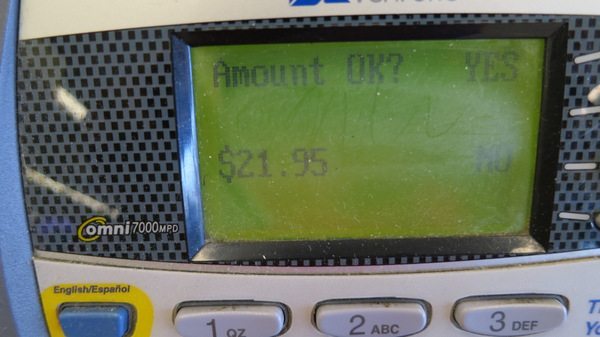

CASH BACKI then went back to Dillon’s and tried to get cash back with a small purchase. But the transaction would not go through if I wanted cash back. But I could make purchases with a PIN if I did not choose the cash back option.

I also wasn’t able to get cash back at CVS or Walgreens with these gift cards issued by US Bank.

But I WAS able to get cash back at Wal-Mart! I’m not sure if this will work at all Wal-Marts or not, but it suggests that some stores will let you get cash back with a gift card while others won’t.

MONEY ORDERSI was able to buy money orders at Wal-Mart and Kroger when I used the Visa but NOT the MasterCard as a debit card and entered my PIN number.

But be VERY CAREFUL with buying money orders. Amounts over $3,000 require special documentation and banks are suspicious of folks – and have to file government reports – who deposit a lot of money orders into their bank account. But you can use money orders to pay bills which you otherwise couldn’t pay with a credit card.

LOADING BLUEBIRDI WAS able to load my American Express Bluebird at Wal-Mart using the Visa, but not the MasterCard gift cards with a PIN!

If you can find Vanilla Reload cards at CVS or other shops, you can also buy a Vanilla Reload at CVS and load your Bluebird online via the Vanilla Reload website.

But if you can’t buy Vanilla Reloads at CVS, you could buy a Visa gift card with a credit card. Then go to Wal-Mart and load your Bluebird (up to $1,000 a day). After that, you can use Bluebird to pay bills, write checks etc.

You can load up to $1,000 a day and $5,000 a month to your Bluebird by using a debit card – or gift card with a PIN – at Wal-Mart without a fee.

WAS THIS WORTH IT?It depends on the amount of the gift card (a larger denomination is better since the activation fee remains the same) and how much you value the miles or points which you earn.

I paid a $5.95 activation fee for a $100 gift card & I earned 105.95 miles/points (assuming I used a card which earns 1 mile/point per $1).

This means that I paid 5.62 cents per mile or point (595 cents /105.95 miles earned) which is a very high price per mile/or point. But it was worth it as a test!

My cost would have been 1.18 cents per mile or point if I had bought a $500 denomination gift card. My cost would have been lower if I used a card which gave a category bonus for purchases at that store.

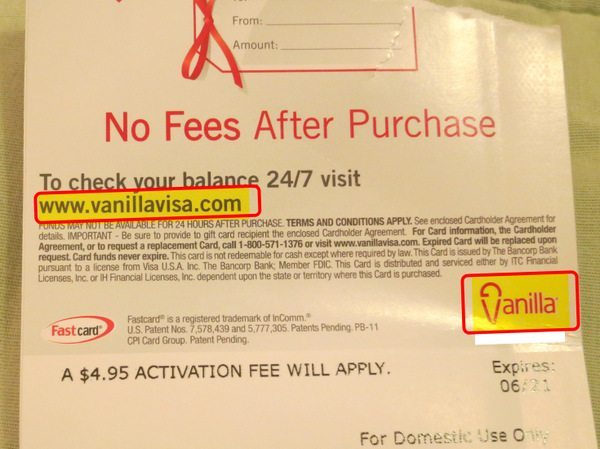

Vanilla Visa Cards Bought at Dillon’s/Kroger & CVS

I bought a $200 Vanilla Visa gift card from Kroger & CVS. You can load between $20 and $500 for a flat $4.95 fee on the Vanilla Visa gift cards. Ideally, I should have loaded $500, but I wanted to make sure that I could use the card with a PIN first, so I bought a lower denomination gift card.

These cards were issued by The Bankcorp Bank and looked like this.

The back of the card looked liked this.

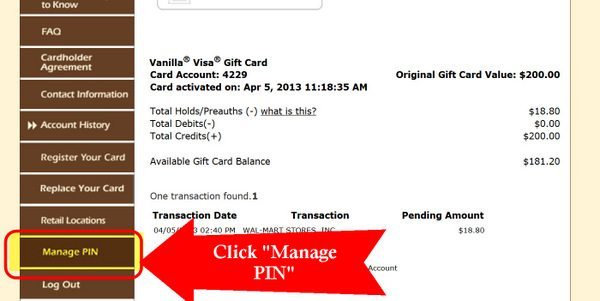

I did NOT get a receipt indicating that I could sign-up for a PIN, nor was there any indication on the card packaging that I could sign-up for a PIN. So I went to the Vanilla Visa website and entered my card number.

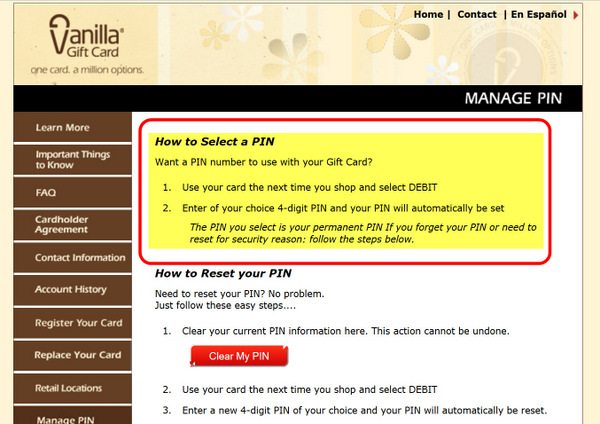

I then noticed a new tab on the left hand side which read “Manage PIN“

The instructions suggested that I could go to a store and select “Debit” and enter in a 4 digit number which would automatically be set as my PIN for future transactions.

But I wasn’t able to make ANY debit purchases at Kroger, Dillon’s, Wal-Mart, CVS & Wal-Greens using a PIN with the Vanilla Visa gift card!

I could make purchases using the Vanilla Visa gift card as a credit card (which is how you normally used a gift card to make a purchase), but couldn’t buy ANYTHING using the card as a debit card with a PIN.

So I called the Vanilla Visa helpline and a few reps told me that I couldn’t use the card as a debit card and that there was no way to get a PIN.

Finally, one rep acknowledged that you can’t – currently – use the Vanilla Visa gift card as a debit card with PIN. But she mentioned that I would “soon” be able to use it as a debit card with a PIN and that they haven’t activated the PIN function as yet.

I can’t wait for this to happen soon and will report back!

Other Experiments

I’m experimenting with other gift cards and will post updates of what works and what doesn’t.

There are lots of Visa and MasterCard gift cards, so please share your experiences in the comments!

Bottom Line

Having a PIN with a Visa or MasterCard gift card opens up lots of possibilities. But I’d use this only to complete the minimum spending requirement on cards and to make payments which I otherwise couldn’t make using a credit card.

Resist the temptation to go overboard! And do the math to see if this works for you! I’d also only buy a SMALL denomination gift card first, to see if this works for you, since there seems to be differences based on where you use the gift card and which bank issued the gift card.