Did Your Credit Card Annual Fee Increase? Don’t Fret – You’ve Got Options!

Signing up for credit cards through partner links earns us a commission. Terms apply to the offers listed on this page. Here’s our full advertising policy: How we make money.

Update: One or more card offers in this post are no longer available. Check our Hot Deals for the latest offers.

INSIDER SECRET: Picking up the phone and calling the bank for a retention offer is one of the best ways to offset a credit card annual fee increase. No guarantees, but you don’t get if you don’t ask!

It doesn’t happen very often, but banks can increase the annual fee on your credit card as long as they give you at least 45 days notice. Usually this is in conjunction with a card “refresh” or update of benefits and perks.

We’ve seen this recently with the Marriott Bonvoy Business™ American Express® Card, which had an annual fee increase from $95 to $125 (See Rates and Fees) and The Business Platinum Card® from American Express, which raised its annual fee from $450 to $595 (See Rates and Fees). And last year, the Citi Prestige® Card upped its annual fee to $495 from $450.

The information for the Citi Prestige card has been collected independently by Million Mile Secrets. The card details on this page have not been reviewed or provided by the card issuer.

I’ve got 2 of the cards above and their higher annual fees are coming due in the next few months, so I’ll have to make a decision. While nobody likes paying more money (especially us frugal-minded types in the miles and points hobby), situations like these are a good opportunity to reevaluate a card’s perks to see if they’re worth it for you. And even if you decide they’re not, don’t rush to cancel just yet. You might have a couple of other options which I’ll explain.

Here’s what to do if you’re facing a credit card annual fee increase.

A Credit Card Annual Fee Increase Doesn’t Always Mean It’s Time to Cancel

You’ll have some time to make a decision after getting notice of an annual fee increase, so no need to rush. The banks must notify you at least 45 days before the fee change (and most banks give you much more time than that).

Plus, you won’t feel the increase until your next annual fee is due – so it could be months before you have to decide whether to keep paying the fee or cancel the card. Don’t jump to cancel just because the fee has gone up until you consider the factors below.

1. Do the Card’s Benefits and Perks Offset the Annual Fee?

Beyond earning valuable welcome bonuses, the best credit cards for travel usually come with generous benefits and perks that can sometimes more than offset the annual fee.

I’m assessing whether the Marriott Bonvoy Business™ American Express® Card is worth keeping after my annual fee is due. It comes with a free night worth up to 35,000 Marriott Bonvoy points at participating Marriott hotels each card anniversary, and you can earn an additional free night if you spend $60,000 or more on purchases in a calendar year. Even with the increased $125 annual fee, it’d still be fairly easy to get a hotel stay worth more than that if you use your free night at an expensive hotel, especially in big cities or during peak travel times.

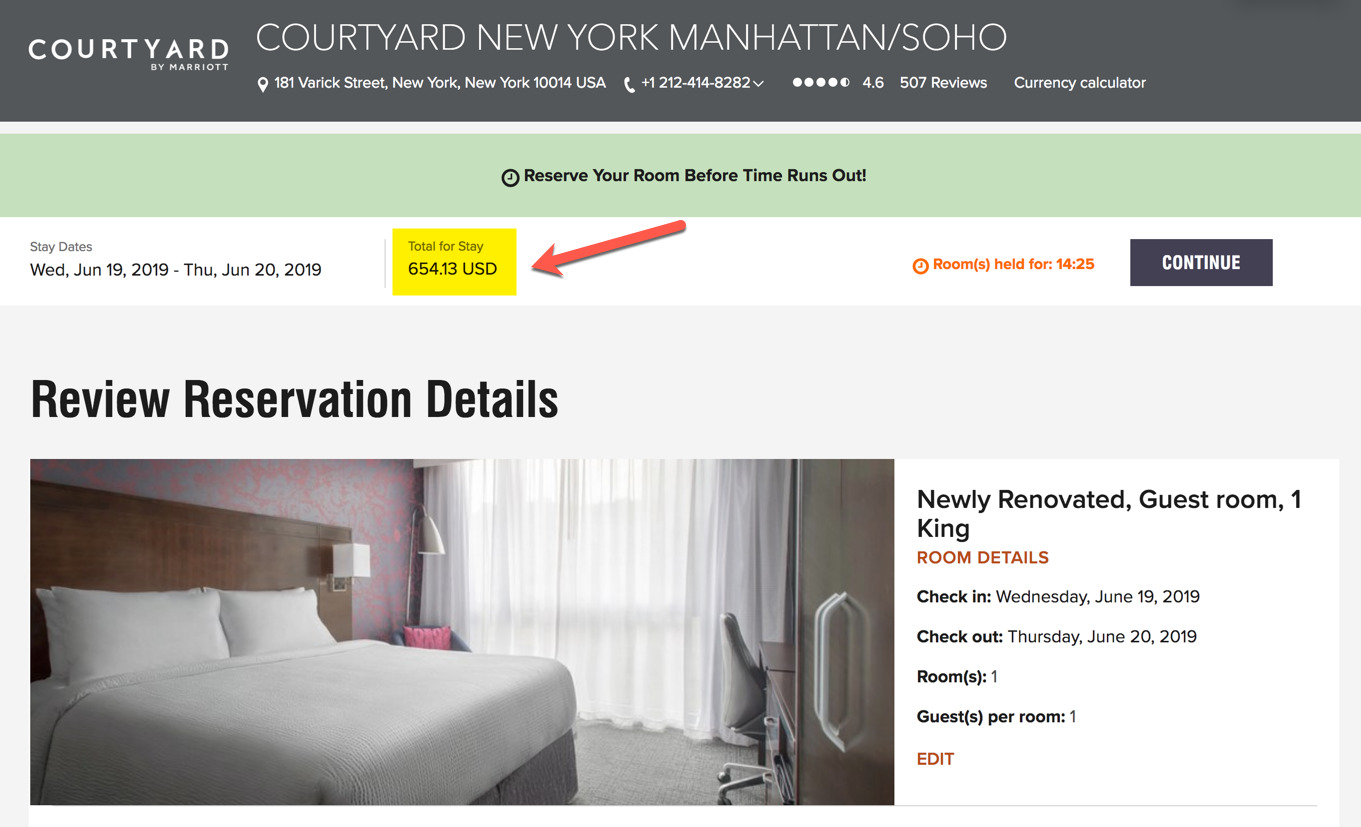

For example, the Courtyard New York Manhattan / Soho costs 35,000 Marriott points per night, but in the busy summer season, charges over $650 if you pay cash.

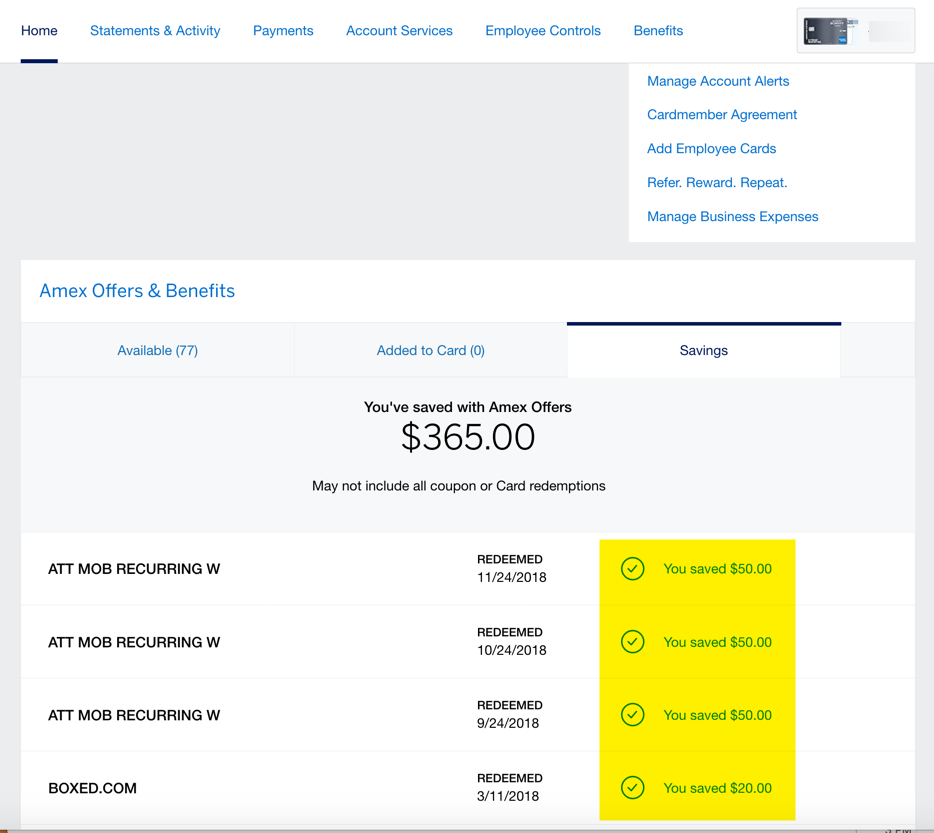

I’m leaning towards keeping my Marriott Bonvoy Business™ American Express® Card after the fee is due, because with this card, I’ve saved $170 using AMEX Offers in the past year or so. These are targeted deals you add to your account to earn discounts or bonus points when you make a qualifying purchase.

A lot of folks have hung on to The Business Platinum Card® from American Express despite its substantial annual fee increase, including team member Meghan. Even though it now costs $595 a year to keep, Meghan’s gotten much more value from the best benefits of the American Express Business Platinum card, including:

- An upgraded room, meals, drinks, and Wi-Fi worth $670 on an AMEX Fine Hotels and Resorts stay at the Loews San Francisco using her AMEX Business Platinum perks

- A $354 discount off a Smart TV by stacking the AMEX Business Platinum annual Dell credit with other online deals (over 50% off)

- Savings of 123,980 AMEX Membership Rewards points (enough for 4 round-trip tickets) with the 35% AMEX Membership Rewards points rebate with the Business Platinum

- The AMEX Business Platinum airline incidentals fee credit, which saved Meghan’s mom $200 on pet transportation fees with United Airlines

For Meghan, this card is a no-brainer. You’ll have to run similar numbers to see if a particular card’s benefits and perks are worth it for you.

2. Ask for a Retention Offer

If you’re trying to decide whether to keep or cancel, it’s always worth calling the number on the back of your card and asking the bank for a retention offer. Sometimes banks will provide incentives for you to keep a card open, like a statement credit or bonus points – especially if you’re a long-term customer. They don’t want to lose your business!

I’ve personally had success with Citi by calling and explaining my reasons for wanting to cancel the Citi Premier Card. They were able to offer statement credits after I met a small spending requirement to effectively discount my credit card annual fee to $0.

Team member Meghan is on a roll – she got a nice boost with a 10,000 AMEX Membership Rewards points retention bonus when she called about her AMEX Business Platinum card. Plus, she got a Citi retention offer and had the annual fee waived on her CitiBusiness® / AAdvantage® Platinum Select® Mastercard®.

The information for the CitiBusiness AAdvantage Platinum card has been collected independently by Million Mile Secrets. The card details on this page have not been reviewed or provided by the card issuer.

I can’t promise the bank will offer anything, but it never hurts to call and ask.

3. Downgrade to a No-Annual-Fee Card

It may be possible to downgrade your current card to a credit card with no annual fee. This is particularly valuable if you’ve had a card for a long time, because when you downgrade, all your existing account information transfers to the new card, including the account number, credit line, payment history, and length of time you had the card open. Your average length of credit history is a factor in calculating your credit score.

For example, if you’re not happy with the increased annual fee on your Citi Prestige card and you decide not to keep it, you may have the option to product change it to the no-annual-fee Citi Rewards+® Card instead, which also earns Citi ThankYou points.

Not every card is eligible to downgrade, and it’s not automatic. The bank will review your account for eligibility, and you’re usually required to have the card open for 1 year before making a change.

4. Consider a Different Travel Credit Card

Deciding if you should keep or cancel a card is a good time to assess your entire travel credit card lineup and see if there are other cards that offer benefits and perks better suited to your spending and travel style.

Here’s a good example: A lot of us are struggling with Citi Prestige changes to the annual fee (going up to $495 from $450) and other benefits, but they did add a very compelling 5X Citi ThankYou points per $1 on dining, where many folks spend a lot of money. If you’re in the same boat, you might consider other cards with similar earning rates at restaurants, like:

- Capital One Savor Cash Rewards Credit Card – Unlimited 4% cash back on dining, entertainment, popular streaming services; $300 cash bonus after spending $3,000 on purchases in the first 3 months of account opening, $95 annual fee.

- American Express® Gold Card – 4X AMEX Membership Rewards points per $1 at restaurants, 35,000 AMEX Membership Rewards points after spending $4,000 on purchases in the first 3 months of account opening, $250 annual fee (See Rates and Fees)

The information for the Capital One Savor Cash Rewards card has been collected independently by Million Mile Secrets. The card details on this page have not been reviewed or provided by the card issuer.

You can check out our updated list of the best credit cards for travel to see if there’s a card that’s a better fit for you.

Bottom Line

A credit card annual fee increase is never fun, even if it’s just a few dollars. Before you decide whether to pay the new annual fee or cancel the card, consider:

- Assessing the card’s benefits to see if they offset the annual fee. This is particularly important if the bank has added new perks or features as part of a card refresh

- Calling the bank and asking for a retention offer. Extra miles or a statement credit can make the card worth keeping

- Downgrading to a no-annual-fee credit card to keep your length of credit history (this isn’t always possible)

- Applying for a different travel credit card that has similar spending categories or benefits

Team member Meghan kept her AMEX Business Platinum even with a hefty annual fee increase, because she gets much more value from the card than the annual fee costs. I’m leaning in favor of hanging on to my Marriott Bonvoy Business AMEX, which had a more modest fee increase, because the annual free night is still potentially worth hundreds of dollars more than the yearly expense.

For more on opening, canceling, and downgrading credit cards, have a peek at these posts:

- Why team member Joseph is going to downgrade credit cards to maintain his credit score and save on annual fees

- Don’t cancel your Chase credit card – downgrade it instead!

- To downgrade or not to downgrade – keep and cancel aren’t your only options

- Think opening credit cards will hurt your credit score?

Don’t forget to subscribe to the Million Mile Secrets daily email newsletter for more tips, tricks, and insights into traveling for free.

For the rates and fees of the Marriott Bonvoy Business American Express Card, please click here.

For the rates and fees of The Business Platinum Card from American Express, please click here.

For the rates and fees of the American Express Gold Card, please click here.

Editorial Note: We're the Million Mile Secrets team. And we're proud of our content, opinions and analysis, and of our reader's comments. These haven’t been reviewed, approved or endorsed by any of the airlines, hotels, or credit card issuers which we often write about. And that’s just how we like it! :)

Join the Discussion!